by Bruce Warner | Oct 3, 2025 | Blog

If your business takes advantage of the Research and Development (R&D) Tax Credit you’ll want to pay close attention to the latest announcement from the IRS. The agency is making important adjustments to its reporting requirements—specifically regarding Form...

by Bruce Warner | Sep 5, 2025 | Blog

On August 28, 2025, IRS issued Rev. Proc. 2025-28 relating to the R&D tax credit and R&D expenses under Section 174. Under this new procedure, if you qualify as an Eligible Small Business (gross receipts average of less than $31 million for the period...

by Bruce Warner | Jul 7, 2025 | Blog

On July 4th, 2025 the President signed into law the One Big Beautiful Bill (OBBB) Act which has many positive aspects for the R&D credit and R&D expensing; notably, the key changes are: The OBBB Act brings significant changes to how businesses can handle...

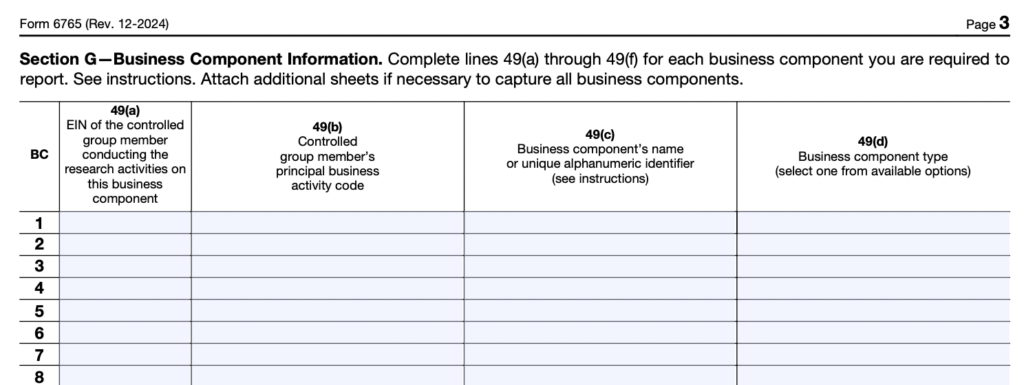

by Bruce Warner | Mar 12, 2025 | Blog

The IRS has significantly revised Form 6765, used for claiming the Research and Development (R&D) tax credit / research credit , introducing new requirements that will impact businesses seeking this valuable benefit. While aimed at enhancing reporting clarity, the...

by Bruce Warner | Jan 14, 2025 | Blog

Although the new Form 6765 R&D tax credit/research credit form is technically not mandatory until tax year 2025, many of our clients are preparing for these changes which are summarized below In 2024, the IRS released a revised Form 6765, which introduces...